Table of Contents

- SUV buyer demographics statistics at a glance

- SUV buyer age and generation statistics

- SUV buyer gender statistics

- SUV family and household demographics statistics

- SUV segment and market mix statistics

- SUV income and education statistics

- SUV occupation and lifestyle segment statistics

- Prospective SUV buyer trends and usage intent statistics

- Historical SUV demographic benchmarks: race, representation, and older comparison points

SUV buyer demographics statistics at a glance

SUVs may feel like the default family car in America, but the buyer profile is more specific than many marketers assume.

The latest SUV buyer demographics statistics show a category led by Gen X and Baby Boomers, tilted toward married homeowners, and split in surprisingly different ways by vehicle size.

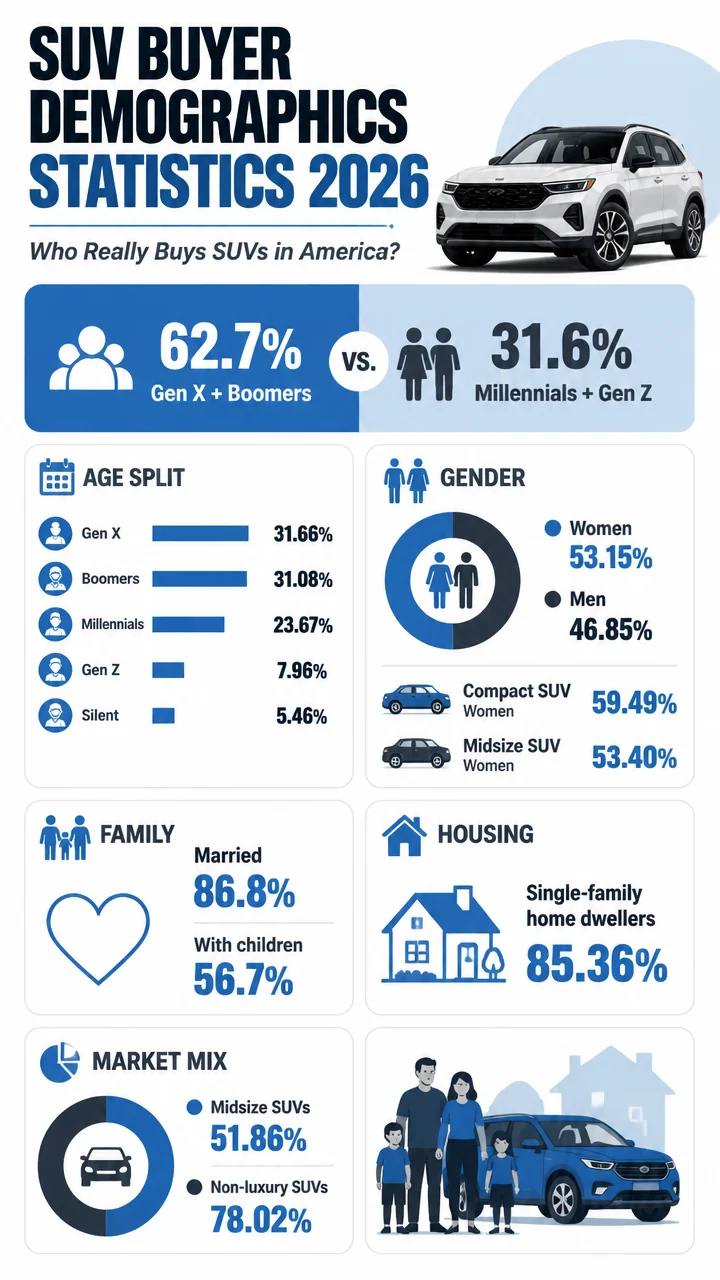

Big number: 62.7% of new retail SUV registrations went to Gen X and Baby Boomers combined, while Millennials and Gen Z together accounted for 31.6%.

At a glance

- 51.86% of new retail SUV registrations were midsize SUVs.

- 53.15% of new retail SUV registrations went to women overall.

- 86.8% of new retail SUV registrations came from married buyers.

- 56.7% of new retail SUV registrations came from buyers with children.

- 85.36% of new retail SUV registrations came from single-family home dwellers.

- 78.02% of registrations were non-luxury SUVs.

Table of contents

SUV buyer age and generation statistics

Gen X was the single largest generation among new retail SUV buyers at 31.66%, narrowly ahead of Baby Boomers at 31.08%.

That near tie matters because it shows the SUV market is still overwhelmingly anchored by middle-aged and older consumers.

Millennials accounted for 23.67% of new retail SUV registrations in the trailing 12 months, while Gen Z contributed just 7.96%.

The Silent Generation still represented 5.46%, which means even the oldest buyers retained a measurable share.

Key takeaway: The center of gravity in SUV demand is not the youngest buyer.

It is the established household buyer, especially Gen X and Boomers.

| Generation | Share of New Retail SUV Registrations |

|---|---|

| Gen X | 31.66% |

| Baby Boomers | 31.08% |

| Millennials | 23.67% |

| Gen Z | 7.96% |

| Silent Generation | 5.46% |

Together, Gen X and Baby Boomers made up 62.7% of all new retail SUV registrations. By comparison, Millennials and Gen Z combined for 31.6%.

That is roughly a two-to-one advantage for the older pair of generations.

Older-skewing demand also appears in broader age data.

In 2019, 43% of new SUV buyers were ages 25 to 54, while 26% were 55 to 64 and 31% were 65 and older.

Less than 1% were age 24 and younger.

YouGov’s more recent intent data points in the same direction.

SUV preference rises with age: 32% among adults 18 to 29, 38% among ages 30 to 44, 42% among ages 45 to 64, and 49% among adults 65 and older.

Why it matters: SUV demand is broad, but it strengthens as consumers age.

That makes SUVs especially attractive to brands targeting established households, repeat buyers, and higher-equity trade-in shoppers.

- 34% of prospective SUV buyers were ages 30 to 44.

- 17% of prospective SUV buyers were ages 18 to 29.

- 16% of prospective SUV buyers were ages 65+.

- Adults 65+ were more likely to plan for an SUV than sedan purchase: 16% vs.

10%.

SUV buyer gender statistics

Women represented 53.15% of total new retail SUV registrations, compared with 46.85% for men.

That is one of the most notable findings in the current dataset because older SUV stereotypes often lean male.

The gender story changes sharply by SUV size.

In compact SUVs, women held a commanding lead at 59.49%, while men accounted for 40.52%.

In midsize SUVs, women still led at 53.40% versus 46.60% for men.

Large SUVs flipped the pattern.

Men represented 51.67% of new retail large SUV registrations, while women made up 48.34%.

| SUV Segment | Women | Men |

|---|---|---|

| Total SUV | 53.15% | 46.85% |

| Compact SUV | 59.49% | 40.52% |

| Midsize SUV | 53.40% | 46.60% |

| Large SUV | 48.34% | 51.67% |

Fast fact: Compact SUVs are the most female-skewing SUV subsegment in the current retail registration data.

Historical and survey benchmarks are more mixed.

Hedges Company data from 2018-2019 showed new SUV buyers at 57% male and 43% female, while Cox owner data showed SUV owners at 54% male and 46% female.

YouGov’s prospective-buyer data is closer to parity, with 52% men and 48% women planning to buy an SUV.

Model and segment examples also show meaningful variation.

Cox data found compact SUV shoppers split evenly at 50% male and 50% female, while mid-size SUV shoppers were 63% male and 37% female.

J.D.

Power research put midsize SUV buyers at 57% male in one segment view and 56% male in another.

Yet Kia Sorento owners were 54% women, compared with 43% for the midsize SUV segment overall in that profile.

SUV family and household demographics statistics

Married buyers accounted for 86.8% of overall new retail SUV registrations.

Single or unmarried buyers represented only 13.12%, making marriage one of the strongest demographic markers in the category.

The marriage effect gets even stronger in large SUVs.

91.9% of new large SUV registrations came from married buyers, while single or unmarried buyers made up 17.63% of large SUV registrations.

In compact SUVs, single or unmarried buyers accounted for just 8.14%.

Pull quote: Nearly 9 in 10 new retail SUV registrations came from married buyers.

Parent status also shows a family-heavy buyer base.

Buyers with children accounted for 56.7% of new retail SUV registrations, compared with 43.29% for buyers without children.

Within subsegments, buyers with children represented 34.50% of compact SUV registrations and 45.43% of large SUV registrations.

Even where the share dips, families remain central to the SUV category’s identity.

Housing data reinforces the same story.

85.36% of new retail SUV registrations came from single-family home dwellers, versus 13.70% from multi-family dwelling residents.

The single-family share rose to 90.69% in compact SUVs and was still a dominant 81.68% in large SUVs.

- 86.8% married overall

- 91.9% married among large SUV buyers

- 56.7% buyers with children overall

- 85.36% single-family home dwellers overall

- 90.69% single-family home dwellers in compact SUVs

Older benchmark data supports this household profile.

Hedges Company found 93% of new SUV buyers owned their home.

SUV segment and market mix statistics

Midsize SUVs dominated the market with 51.86% of new retail SUV registrations.

Compact SUVs accounted for 28.77%, while large SUVs represented 19.36%.

| SUV Type | Share of New Retail SUV Registrations |

|---|---|

| Midsize SUV | 51.86% |

| Compact SUV | 28.77% |

| Large SUV | 19.36% |

Non-luxury SUVs made up 78.02% of new retail SUV registrations, while luxury and exotic SUVs represented 21.91%.

That split suggests the category is still driven primarily by mainstream rather than premium demand.

At a glance: The typical SUV buyer is most likely shopping in the midsize, non-luxury part of the market.

Income benchmarks differ by subsegment.

Cox Automotive data from 2018 showed compact SUV shoppers with a median household income of $65,000, while mid-size SUV shoppers had a median income of $70,000.

J.D.

Power’s midsize segment profiles are significantly higher, with median household income figures of $109,901 and $116,933 in two separate views.

Age also varies by segment benchmark.

Cox data put the median age at 58 for compact SUV shoppers and 54 for mid-size SUV shoppers.

J.D.

Power’s midsize SUV segment research found median ages of 54 and 56 years.

SUV income and education statistics

SUV buyers skew relatively affluent. Hedges Company data found 40% of new SUV buyers had household income of $100,000 or more.

Another 10% fell in the $75,000 to $99,999 range, 19% were in the $50,000 to $74,999 bracket, and 31% were under $50,000.

Strategic Vision’s 2020 data estimated the median household income of new SUV buyers at $97,082, another sign that SUVs over-index with upper-middle-income households.

| Income Group | Share of New SUV Buyers |

|---|---|

| $100,000+ | 40% |

| $75,000-$99,999 | 10% |

| $50,000-$74,999 | 19% |

| Under $50,000 | 31% |

Prospective buyer data also shows SUVs indexing above sedans among higher-income consumers.

YouGov found higher-income consumers made up 15% of prospective SUV buyers, versus 10% of prospective sedan buyers.

Lower-income adults made up 41% of prospective SUV buyers, compared with 53% of prospective sedan buyers.

Education levels are similarly elevated.

According to Strategic Vision data, 53% of prospective SUV buyers had a bachelor’s degree or higher, 28% had some college education, and 18% were high school graduates.

Why it matters: SUVs are not exclusively premium products, but the audience leans toward educated, higher-income households more than many passenger-car segments.

SUV occupation and lifestyle segment statistics

Professional occupations represented the largest buyer share at 18% among new retail SUV buyers.

Management followed at 17%, while blue-collar occupations and “other” occupations each represented 16%.

Retired buyers made up 15% of new retail SUV registrations, which fits the broader age skew seen throughout the category.

Office and admin workers represented 7%, sales occupations 6%, and technical occupations 5%.

| Occupation Group | Share of New Retail SUV Buyers |

|---|---|

| Professional | 18% |

| Management | 17% |

| Blue-collar | 16% |

| Other | 16% |

| Retired | 15% |

| Office/Admin | 7% |

| Sales | 6% |

| Technical | 5% |

Experian’s Mosaic lifestyle segmentation adds another layer.

Philanthropic Sophisticates (Mosaic C13) ranked as the #1 lifestyle segment among new retail SUV buyers.

American Royalty (Mosaic A01) ranked #2, and Fast Track Couples (Mosaic F22) ranked #3.

- Philanthropic Sophisticates: 3.34% of U.S. individuals among new retail SUV buyers

- American Royalty: 2.26%

- Fast Track Couples: 4.92%

Preferred marketing channels vary by segment.

Email was the preferred marketing channel for the top two lifestyle segments, while text messaging was preferred for Fast Track Couples.

Fast facts: The top lifestyle segments signal a buyer base that is affluent, established, and highly targetable through direct digital outreach.

Prospective SUV buyer trends and usage intent statistics

40% of American adults planning to buy a vehicle in the next 12 months said they were likely to get an SUV. Since only 26% of American adults planned to buy or lease a vehicle at all, that indicates SUVs remain one of the strongest default choices inside the active purchase market.

Channel and shopping behavior data also suggest a relatively dealership-friendly path to purchase.

53% of prospective SUV buyers considered franchise dealerships, versus 46% of prospective sedan buyers.

Broader market-shopping data supports SUV dominance.

Cox Automotive found that two-thirds of non-luxury vehicle shoppers considered an SUV in Q3 2022.

In the digital shopping environment studied during COVID-19, 52% of SUV shoppers said a deal or incentive would move them to transact.

That makes pricing and promotional strategy especially relevant even in a category with strong baseline demand.

- 40% of in-market vehicle buyers are likely to choose an SUV.

- 53% of prospective SUV buyers considered franchise dealerships.

- 52% of SUV shoppers said incentives could move them to transact.

- Two-thirds of non-luxury shoppers considered an SUV.

Historical SUV demographic benchmarks: race, representation, and older comparison points

Strategic Vision found 23% of SUV buyers identified as belonging to a racial or ethnic minority group in 2020, compared with roughly 40% of the overall U.S. population.

That gap stands out as one of the clearest representation imbalances in the dataset.

Cox registration data from 2018 showed compact SUV buyers as 74% Caucasian, 4% Hispanic, 4% African American, and 3% Asian.

Mid-size SUV registrations were 70% Caucasian, 5% Hispanic, 6% African American, and 2% Asian.

| Race/Ethnicity Benchmark | Compact SUV | Mid-size SUV |

|---|---|---|

| Caucasian | 74% | 70% |

| Hispanic | 4% | 5% |

| African American | 4% | 6% |

| Asian | 3% | 2% |

Political identity appeared in one 2020 benchmark as well: Republicans held a 55% share of the U.S. sport-utility market among surveyed new SUV buyers.

These historical snapshots should not be read as universal for every model or subsegment, but they help explain why SUV buyer demographics often correlate with suburban homeownership, established household income, and older age bands.

Notable findings

- Women now lead total new retail SUV registrations, driven heavily by compact SUVs.

- Gen X and Baby Boomers control nearly two-thirds of the market.

- Married buyers dominate SUV retail demand at 86.8%.

- Midsize SUVs are the core of the category, accounting for more than half of registrations.

- Single-family homeowners remain the dominant household profile.

- Higher income and higher education continue to over-index in SUV demand.